The CRA has made sweeping changes to Canada’s “tax amnesty” initiative, the Voluntary Disclosures Program (VDP). This overhaul fundamentally changes who is eligible and the financial relief available to taxpayers who come forward ‘voluntarily’ and submit unfiled returns or rectify past omissions or mistakes made on previously filed tax returns.

Detailed information on the updated rules, which apply to VDP applications received on or after October 1, 2025, is available in CRA’s information circular IC00-1R7 and in GST/HST Memorandum 16-5-1. Files received before that date are assessed under the previous rules (which you can find in circular IC00-1R6 and Memorandum 16-5).

This chart and bulleted list are high-level summaries of the changes. Below them is an in-depth analysis of the revamped Voluntary Disclosures Program by the VDP experts at Faris CPA, one of Canada’s top tax consultant accounting firms.

| Old – IC00-1R6 (2017) | New – IC00-1R7 (2025) | Analysis | |

| Categories | Two streams/categories: “General” and “Limited”. | Old streams changed to “Prompted” and “Unprompted”. | Simpler for taxpayers to understand and less ambiguous rules for eligibility. |

| Eligibility Threshold | Very high: ineligible if “enforcement action” had occurred, i.e., being contacted by the CRA. | Now, only an active audit or investigation prevents a taxpayer from being eligible. | In cases where the CRA has sent certain types of communications, e.g., a notice about an error on a return or a request to correct an issue, a taxpayer is not “barred” from relief, but can still benefit from a Prompted disclosure. |

| Penalty Relief | Under the General Program, all penalties are waived; under the Limited Program, only gross negligence penalties are waived. | Unprompted: all penalties waived. Prompted: Discretionary relief from CRA, up to a 100% waiver of penalties is still available. | Even files where ‘enforcement action’ (as defined under the previous regime) has taken place, a taxpayer can still be offered full relief from administrative penalties. |

| Interest Relief | General Program: Typically 50% interest relief on taxes owing for returns over three years old. No interest relief on taxes owing in returns of the three most recent years. Limited Program: no interest relief. | Unprompted: 75% interest relief (all years). Prompted: 25% interest relief (all years). | Clearer relief standards. Some relief is available even if a taxpayer has been contacted by the CRA. |

| Applicable Taxes | Income Tax, Payroll Tax, GST/HST, Air Travel Security Charge, Softwood lumber export charges. | Addition of Luxury Tax, Digital Services Tax, Underused Housing Tax, and Global Minimum Tax. | More relief under additional taxing statutes that have been folded into the new VDP regime. |

- VDP Categories. The old “General” and “Limited” streams are replaced with “Unprompted” and “Prompted,” making eligibility easier and clearer.

- Eligibility. Previously, any CRA contact barred access; now, only an active audit or investigation does. Certain CRA communications may still allow relief under the “Prompted” stream.

- Penalty Relief. Under the new rules, accepted unprompted disclosures waive all penalties, while prompted disclosures may still receive discretionary relief from administrative penalties depending on the taxpayer’s factual circumstances.

- Interest Relief. Relief is standardized: 75% for unprompted and 25% for prompted cases, compared to the older system’s limited or no interest relief.

- Applicable Taxes. The program now covers more areas, including the Luxury Tax, Underused Housing Tax, and Global Minimum Tax, broadening its scope beyond earlier regimes.

The Need for a Voluntary Disclosures Program

Even well-intentioned Canadians can find themselves behind on their tax obligations. Maybe an old return or tax form was overlooked, or a business deduction was claimed incorrectly. Maybe you’re an Uber driver, Amazon seller, social media influencer, or OnlyFans creator in Canada with years of unreported digital income.

These mistakes don’t always come from bad faith; they can result from misunderstanding the rules, administrative errors, or changes in circumstances. But the consequences of not correcting them can be severe, ranging from interest and penalties to increased CRA scrutiny and tax audits, to criminal charges.

For taxpayers who want to correct the record and get back onside, Canada’s Voluntary Disclosures Program has long been the avenue to do so. An accepted VDP application generally protects a taxpayer from gross negligence penalties and criminal prosecution, and allows for interest and penalty relief. Over time, however, the program has evolved, undergoing major changes to how it works, as it has once again, this time for the better.

Overview of Recent Changes to the VDP

The VDP now includes more taxes than it did under the old system. In addition to income tax, GST/HST taxes, payroll tax, excise duties, and Air Travellers Security and softwood lumber exporting charges, the VDP now also covers reporting deficiencies related to the Underused Housing Tax, luxury tax charged under the Select Luxury Items Tax Act, fuel charges under the Greenhouse Gas Pollution Pricing Act, Global Minimum Tax, and the Digital Services Tax, which was included in the information circular despite the government’s intention to rescind it, as it’s still technically on the books.

Increased Eligibility

Under the “old” system, which still applies to VDP applications received before October 1, 2025, a taxpayer was ineligible for the VDP if the CRA contacted them about a tax issue. The program typically separated disclosures into two streams: the General Program, for less-severe “infractions” that allowed for penalty and partial interest relief, and the Limited Program, for discrepancies that showed an element of intentional non-compliance and offered less relief than in the General track.

There was a great amount of criticism of the previous program that was implemented in 2017, as it eliminated many of the benefits and created a much higher standard for relief than previous iterations. Practitioners had been asking CRA for years to revert to the old standards or update the VDP to make the program a more attractive option for taxpayers.

The CRA has done away with these restrictive eligibility requirements and disclosure classifications in its VDP overhaul. As of October 1, 2025, you can still submit a VDP application (i.e., it may still be considered “voluntary”) even if they’ve contacted you or received information from a third party regarding your possible tax non-compliance.

New Disclosure Categories

The new system classifies disclosures as Unprompted and Prompted. Unprompted applications include those submitted without the CRA contacting the taxpayer in any way and applications made after the taxpayer receives an education letter or notice containing general information on a particular tax-related topic.

Applications are considered Prompted when they’re submitted after the CRA initiates written or verbal communication with the taxpayer about a specific tax compliance issue and sets a deadline for the taxpayer to correct it. A VDP application is also classified as Prompted if it’s received after the CRA is informed by a third party that the taxpayer may be involved in non-compliance.

This is a massive change. Significantly more taxpayers will now be eligible for the VDP and benefit from its financial savings.

Greater Relief Measures

Unprompted applications are normally eligible for “general” relief: 100% penalty relief and 75% interest relief on taxes owing. Prompted applications are normally eligible for “partial” relief: up to 100% penalty relief and 25% interest relief.

This is a vast improvement in the relief allowed in the General and Limited VDP streams. The General Program waives penalties but only grants interest relief up to 50% for returns preceding the three most recent tax years and requires full interest be charged on returns within the three most recent years. The Limited Program provides no interest or penalty relief (aside from the waiving of gross negligence penalties).

Eligibility Clarifications and Carve-Outs

As it is under the older system, to qualify, applications must still be voluntary, relate to periods at least one year past due, and disclose an error or omission with applicable penalties. However, the expanded eligibility also allows taxpayers to apply to the VDP if the issue disclosed doesn’t involve a penalty and only results in interest.

Standardized Documentation Timeframes

The CRA now spells out the documentation periods you’re expected to file with a VDP application package:

- Income tax returns. Supporting documents for the most recent six years, ten years if the issues involve foreign income and asset reporting. Documentation isn’t needed for tax returns that don’t contain errors or omissions.

- GST/HST returns. Supporting documentation is required for the four most recent reporting periods, except for returns without errors or omissions.

This contrasts with the now “old” regime, which required a complete package but did not specify a fixed “six-year/ten-year” or “four-period” documentation timeline in the same explicit way. (The CRA can request older documents as needed.) These standardized windows make expectations clearer and reduce the likelihood of back-and-forth with the CRA.

Scenarios that Make a Taxpayer Ineligible for the Voluntary Disclosures Program

The circular lists scenarios that are not eligible for the VDP, including:

- The taxpayer, or a related taxpayer, is being audited or is under investigation by any federally- or provincially-regulated authority for issues related to the disclosure

- Applications where the return in question produces a refund and no taxes or penalties are owing

- A VDP application seeking relief on previously assessed penalties and/or interest

- Attempts to make or amend elections

- Applications that involve insolvency (e.g., bankruptcy)

- Matters tied to advance pricing arrangements with the CRA or another tax authority inside or outside Canada

These carve-outs are more streamlined and provide clearer guidelines than those in IR-006.

What Stayed the Same (High Level)

Some anchors remain: relief is discretionary, protection from prosecution applies when relief is granted, and the CRA may audit or verify disclosures even when accepted. Rights of redress also remain the same and are available via second administrative review and judicial review, while objections to the discretionary relief decision itself are not available; unchanged in substance from prior guidelines. (More on this below.)

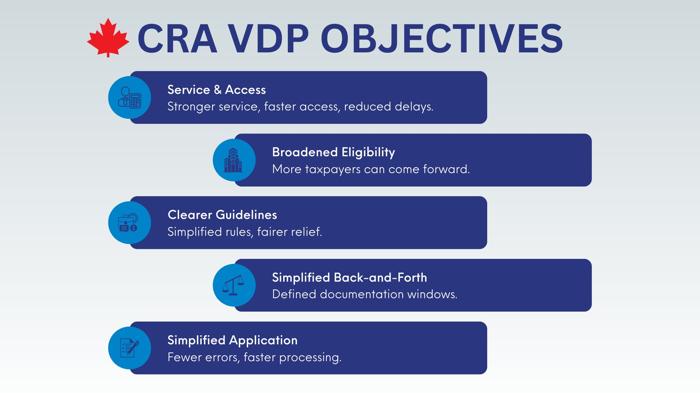

Objectives Behind the Changes

The headline objective is service: the federal minister has directed the CRA to deliver a 100-day plan to “strengthen services, improve access, and reduce delays.” The VDP refresh aligns with that mandate by explicitly aiming to make corrections easier and the program more accessible.

Broaden Eligibility so More People Can Come Forward

Under IC00-1R6, many forms of CRA contact tended to push applicants out of the standard relief pathway or render a disclosure non-voluntary; by contrast, the September 2025 guidance clarifies that education letters (general outreach providing guidance) do not make a disclosure “prompted,” and that taxpayers “prompted” by more specific communications would now be eligible.

That broadened gateway is the key policy shift: it encourages more taxpayers to come forward. That said, however, it’s not worth risking a denial. Talk to our VDP experts at Faris CPA and drastically increase your chances of acceptance into the Program to benefit from the financial relief it provides.

Clarify and Standardize Relief & Guidelines

The new framework replaces the old “General vs. Limited” tracks with the transparent and more clearly defined Unprompted and Prompted system. Along with increasing eligibility for the VDP, this transformation addresses another key criticism levied at the CRA, this one by Canada’s Taxpayers’ Ombudsman in June 2025, that the CRA needs to provide information that is more “relevant, clear, concise and easy to find.”

Reduce Back-and-Forth with Clear Documentation Windows

The new, more specific guidance on documentation that should be included in a VDP application will likely also reduce delays in service.

Simplifying the Intake Experience

The CRA will release a simplified Form RC199 on October 1, 2025. A simpler application reduces errors at intake and shortens the time between filing and a decision.

Provide One Door for Multiple Tax Regimes

Finally, the CRA explicitly positions the revamped VDP as a unified on-ramp across a wider slate of statutes and taxes. For individuals and businesses with mixed obligations, a single system is simpler to navigate.

Implications for Taxpayers

The broadened eligibility rules mean Canadian taxpayers who may have hesitated in the past now have a genuine opportunity to make things right before the situation escalates into an audit or investigation. Other outcomes include:

Relief Is No Longer Guesswork

The introduction of fixed percentages and clearer guidelines on how VDP applications are categorized removes the uncertainty that taxpayers often faced under the old “General” and “Limited” tracks. This allows you to plan with greater accuracy: you can quantify potential savings and model cash flow impacts.

Acting Early Still Matters

Even though more taxpayers qualify, the timing of your disclosure directly affects the outcome. The longer you wait, the more likely it is that the CRA will reach out to you first, putting you in the Prompted track, where the financial benefit drops significantly. For taxpayers with multiple years of outstanding obligations, the reduced interest relief can translate into thousands of dollars.

A much worse scenario, however, is also more likely the longer you wait: a CRA tax audit or an investigation by a regulatory body that disqualifies you from the program altogether.

Protecting Reputation and Reducing Risk

Perhaps the most personal implication is peace of mind. An accepted VDP application still offers protection from prosecution, which is particularly valuable for business owners whose reputation could be damaged by a public trial.

An Example of the Potential Financial Savings Available in the New VDP

Please note that the VDP does not erase the underlying tax owed, and relief is discretionary. The CRA will still expect full payment of principal tax amounts, and incomplete or inaccurate applications risk rejection.

With that being said, we’ve created a hypothetical example to help demonstrate the potential financial savings possible under the new VDP rules compared with the old system and a rejected VDP application. This example uses the following assumptions of fact:

- The taxpayer is an Ontario resident for all years.

- The marginal tax rate (federal + Ontario) is approximately 46% for each year.

- The taxpayer had unreported income of $100,000 in each taxation year 2015-2024.

- All $100,000 per year is fully taxable at the top marginal rate.

- All returns are filed simultaneously after October 1, 2025.

- All amounts are rounded to the nearest $100.

- Prescribed interest rates are based on historical CRA rates for each year, compounded daily.

- Penalties include late-filing penalties [Income Tax Act (ITA) 162(1)], repeated failure to report income penalties (ITA s.163(1)), and gross negligence penalties (ITA s.163(2)), as applicable. Note that where gross negligence penalties (GNPs) are assessed, repeated failure to file penalties generally won’t be, since repeated failure to file penalties can actually be larger than GNPs, as they stack year-over-year.

- No VDP relief is granted except as specified in each scenario, which are: old program, new program, no relief and no GNPs, and no relief and GNPs.

- No other deductions, credits, or offsets are considered.

| Scenario | Tax | Penalties | Interest | Total Cost |

| (a) 50% interest relief 2015–2022, all penalties vacated (old General Program) | $208,000 | $0 | ~$60,000 | ~$268,000 |

| (b) 75% interest relief for all years, all penalties vacated (new program) | $208,000 | $0 | ~$30,000 | ~$238,000 |

| (c) No relief, all penalties and interest apply (old Limited Program) | $208,000 | ~$208,000 | ~$120,000 | ~$536,000 |

| (d) No relief, gross negligence penalties also assessed | $208,000 | ~$104,000 | ~$120,000 | ~$432,000 |

So in this case, we have almost a $30k reduction in total tax cost under the Unprompted Program when compared with the General Program. Also of note is the massive savings of an accepted VDP application in the new system compared to the old Limited Program or a rejected disclosure.

The bottom line: take advantage of this opportunity as quickly as possible.

Process for Making Disclosures

A VDP application begins with Form RC199. Starting October 1, 2025, a simplified version of this form will be available, designed to reduce confusion, errors, and delays. Alongside the form, taxpayers are expected to provide all supporting information relevant to the disclosure as discussed earlier.

Applicants can submit the form electronically through My Account, My Business Account, or Represent a Client, or by mail to the CRA’s designated intake centres. Before filing, taxpayers can also request a pre-disclosure discussion. These discussions are informal and non-binding, but they allow taxpayers or their representatives to test whether a situation would likely qualify for relief before making a full disclosure. Speak to us first, before scheduling a discussion, if you’re considering this option.

Completeness and Accuracy

A disclosure must be complete to be valid. The CRA expects taxpayers to identify all errors, omissions, and non-compliance within the scope of their application. Partial disclosure, such as reporting one unfiled year but not others, can result in rejection. (Which underscores the importance of having a professional handle your application.) Where a taxpayer cannot immediately provide all records, the CRA may, at its discretion, allow a grace period to complete the submission, but this is not guaranteed.

How the CRA Makes Its Decision

Once an application is received, the CRA assesses it against the eligibility requirements set out in IC00-1R7. These include whether the disclosure is voluntary, whether it involves a penalty or interest exposure, and whether it relates to a period more than one year past due.

The CRA has broad discretion to grant or deny relief. Importantly, acceptance into the program does not prevent the CRA from auditing or verifying the information provided. A disclosure that is accepted means the taxpayer avoids prosecution and secures the stated relief, but it does not shield them from future scrutiny.

Communication of the Outcome

After review, the CRA issues a written decision. If relief is granted, the decision will confirm the penalties waived and the percentage of interest relief applied. If the application is denied, the taxpayer will be notified of the reasons. In either case, the CRA may reassess returns or accounts to reflect the corrected information and issue new balances due.

Rights of Redress

While VDP decisions are discretionary, taxpayers are not without recourse if they disagree with an outcome. There are two key avenues of redress:

- Second Administrative Review. Taxpayers can request that another CRA official, independent of the initial decision-maker, conduct a second-level review of the file. This allows the taxpayer to present additional information or clarify issues that may not have been fully considered.

- Judicial Review. If the taxpayer still disagrees after a second review, they can apply to the Federal Court for judicial review. This process does not re-argue the facts of the case but examines whether the CRA acted fairly and reasonably in exercising its discretion.

It’s important to note that you cannot file an objection under the Income Tax Act against a discretionary VDP decision. Objections are still an option, however, for any reassessments of tax amounts that flow from the disclosure itself.

Practical Considerations

The implications are clear: submitting a strong, accurate, and complete disclosure package from the start maximizes the likelihood of success and minimizes the need for appeals. Even though redress options exist, the best approach, our approach, is to avoid disputes and escalations by ensuring your initial application is comprehensive, aligned with CRA expectations, and firmly supported by the law.

In Conclusion

An accepted disclosure does more than address mistakes of the past and help you sleep better at night. It also sets you up for a brighter financial future. The modernized VDP, with its emphasis on accessibility and clarity, provides more opportunities and greater financial savings, if you take advantage of them.

Navigating the program still requires careful preparation. Every detail matters, from choosing the right disclosure strategy to compiling supporting records that withstand review.

If you need to submit unfiled returns, disclose unreported income, or fix mistakes on previous returns, speak to us today. We’ll guide you through each step, help you gather all the supporting documentation you need, protect your financial interests, and help you save more of your hard-earned money by making the most of the relief available.